Common Auto Insurance Questions

Here are common auto insurance questions and the answers to them.

The Three Objectives of Auto Insurance

Question: What is the purpose of automobile insurance

Answer: Automobile insurance has three goals.

First, there’s liability. Liability covers damage to other people’s cars and property. Third-party coverage is what you call it because it covers other people.

Auto insurance also pays to protect you and your passengers through collision, comprehensive, or medical coverage. This coverage is also known as first-party insurance.

Finally, insurance can help you adhere to the law. Automobiles can be dangerous, heavy, and expensive pieces of machinery. Insurance protects drivers, passengers, as well as others, from any injury or damage that may be caused by someone who wouldn’t have the means to pay.

Every state has its own requirements for coverage. We can meet our financial obligations under state law by purchasing automobile insurance.

Bodily and property liability insurance coverage

The majority of states require coverage for both bodily injury liability and property damage liability (New Hampshire is an exception).

Insurance Coverage Requirements

Question: What are the essential requirements to be able to drive your car safely on the streets?

Answer: Okay. Let’s begin with the fact that New Hampshire does not require auto insurance coverage. Although most New Hampshire residents buy auto insurance, it is not required by the state.

The majority of states require liability coverage. This covers both bodily injury liability as well as property damage liability. This is a third-party policy. This is the coverage we purchase to protect others. We are responsible for the injuries or damage is done to others by being liable. You often hear numbers like 15/30 or 50/100 coverage. These numbers are used to describe the coverage for bodily injuries you purchase. The first number refers to one person who is injured. If multiple people are hurt, the second number will show how much you’ll be reimbursed.

A third number is also included in this set. For example, 50/100/25. This last number, 25, is $25,000 in property liability. The insurance company will cover up to $25,000 in property damage if you cause damage to someone’s vehicle or fence. The government requires that all citizens have liability coverage in every state except New Hampshire.

Level of liability insurance

Question: What level of liability do you have to assume when purchasing?

Answer: Only the minimum amount is required. The minimum required by each state is different. The most common mandatory personal insurance coverage is 25/50, according to me. For injury to one person, twenty-five thousand dollars. The most common property damage liability is $25,000 per incident.

Uninsured motorist coverage is also required in some states. This coverage protects you in the event you are struck by an uninsured driver or another motorist without coverage. Some states require personal injury protection (PIP). These coverages are known as first-party coverage. They cover your injuries regardless of who was at fault for the accident. This coverage is also known as insurance or no-fault.

State insurance requirements

Question: How can you find out what your state requires?

Answer: You have four options to locate this information. The first is to contact your state’s department of insurance. Second, you can contact the National Association of Insurance Commissioners. Or do a simple internet search. Enter your state and search for “minimum auto coverage.”

You will need to have additional coverage, not by the government but by your car lender. This is called comprehensive and collision coverage. It is required if you don’t own the car (e.g. if you are leasing it or taking out a loan), or if you lease the vehicle.

First party insurance coverage

This is also first-party coverage, which covers damage to your vehicle. These banks and other insurance companies require that you purchase this coverage. They don’t care about what you do. They are concerned about what you do with the car in which they hold a financial interest. If you don’t have the car, you will need collision and comprehensive insurance. It is not required by law but rather by your financial institution.

In some cases, you may be forced to buy insurance at a higher price if you fail to obtain the coverage that you need.

Required insurance coverage

Question: What happens if you don’t buy this coverage?

Answer: Your bank or lender will find out if you don’t purchase it. They have a relationship with the insurer. Then, they will buy it for your loan and charge it to your loan as forced-place insurance. This will not only surprise you, but it will also be much more costly than the coverage that you could get on your own.

Question: Because states don’t require collision and comprehensive coverage, does that mean they have no say over the type of coverage such as what coverage is offered, how much it costs, and so on?

Answer: In regards to collision and comp, the states may determine how much they can charge for it. They might set limits for companies or allow them to set prices in different states based on different regulatory frameworks. Financial institutions are responsible for determining whether you need to have collision and comp. A bank won’t let you purchase a comprehensive policy that has a $5,000 deductible.

Optional insurance coverage

Question: What coverage types might people desire, even though they are not required to have it?

Answer: Uninsured motorist or underinsured driver coverages are required in certain states. These coverages cover your injuries and damage to your car if you are struck by an uninsured motorist or underinsured driver. Because they don’t have any insurance, the driver isn’t responsible for any damage caused.

Uninsured motorist coverage

You could theoretically sue them and take them to court. However, most often, uninsured drivers don’t have the means to pay for insurance. Research has shown that the majority of people driving without insurance don’t do it because they want to follow the man. They can’t afford coverage. It’s also unlikely that they have enough assets to cover the cost of your injuries and damages to your vehicle.

Even if your state doesn’t require it, you should consider purchasing uninsured motorist coverage. You should consider purchasing as much uninsured motorist coverage to your liability coverage. You’re saying that injuries to others are more important than injury to you and your car.

Other types of insurance coverage

Question: Is there another type of coverage that’s not necessary but still worth considering?

Answer: Sure. Another thing people love to think about is rental car insurance. The question “What will I do the next seven to fifteen days while my car is out-of-service after an accident?” can be answered by rental car coverage.

Remember that if someone hits you, their insurance should cover your rental. Without a rider, collision coverage might not cover a rental car if you are at fault.

Make sure to cancel your car insurance policy if you sell your vehicle or change companies.

What about gap insurance

Question: Which types of coverage can be sold that aren’t helpful?

Answer: Guaranteed asset protection, or gap insurance, is what frustrates me the most. This is sold with the undercoating of a new vehicle (basically credit coverage). It covers the difference between the amount you owe and the insurance that will pay for the car if it is totaled.

After you buy your coverage, the car’s worth drops, and then it is totaled. The car still has $18,000 remaining. The insurance company will only pay $15,000. The insurance company will only pay $15,000.

Gap insurance is a very low-loss product. This is because the insurance companies pay a lot less than they receive in premiums.

While there are many people who appreciate it, it is not the only one for whom it is worthwhile. It’s a common fact that we often see it on the lot and people hear about it during sales pitches. It’s a product that is very profitable for insurance companies and not for consumers. This is why I always explain it to people.

Lot gap insurance

Question: You mentioned that you were on the lot and have gap insurance. Is this insurance you have or an alternative type?

Answer: It is interesting that Wells Fargo’s lender got into trouble for selling gap insurance a few years back. This was part of their financing agreement. Although there are mainline insurance companies that offer gap policies, it is often sold separately from your insurer.

I believe that some lenders offer a form of gap insurance for no additional cost with a loan. Gap insurance can be purchased separately through specialty insurance.

Deductibles

Question: Can you tell us what deductibles are and how they work?

Answer: Yes. This covers damage like an accident or damage caused by a shopping cart. You can also claim your car was stolen.

The deductible is the amount that you pay before your auto insurance company pays. It works like this: If your deductible is five hundred dollars and you sustain damage to your vehicle, $500 will be due. The insurance company will pay $500. The deductible is the part that you pay. If the damage is $499 you will pay the entire amount and the auto insurance company will pay zero. Although your deductible can be lower, your premium will still be higher. You can also increase your deductible to pay a lower premium.

What deductible is best

Question: If they are given the option, how do they decide what deductible is best?

Answer: It is important to evaluate the value of any premium benefits they receive. It is important to compare the amount they will save on the front end by increasing the deductible by a few hundred dollars. It’s worth trying it with different deductibles. The rule of thumb is that the lower your deductible can be, the better.

You should also be aware of the fact that your vehicle’s value will decrease over time. Your comprehensive coverage will decrease in value as your car’s value declines. While your premium will decrease, it may be worth considering dropping coverage for a car only worth a few hundred dollars. Consumer Reports suggest that you drop this type of coverage if your annual premiums exceed 10%.

Maintaining maintenance records

Question: What happens if you don’t agree with the amount that the auto insurance company wants? What if your car is worth more than what the insurance company claims?

Answer: It is a good idea to keep your maintenance receipts. You can do the same thing with your car as you would for your home. You should keep a detailed, current record of the condition of your car. What is the mileage? What maintenance was done? To get the full value of your car, you will need to show the condition it was before the accident.

Manufactures keep records

Question: Are manufacturers and dealers keeping records of maintenance and upkeep for newer vehicles with the ability to transmit data?

Answer: Yes, absolutely. Many websites provide information on maintenance, work done and the mileage transmitted to the central computer.

It’s something I enjoy thinking about, to help explain the theory. Imagine a Mazda Miata owner who is in love with their 1992 Mazda Miata. They keep it in perfect condition. A 1992 Miata was also purchased by another person. They take it to the junkyard for spare parts and keep it running.

They are both 1992 Miatas but they are not the same car. The person who loves and maintains the car will get more because it’s more valuable and has the documentation. It’s worth more if you do your bit and keep it in great shape than letting it go to pieces.

Evaluate both Insurance providers and coverage

Question: You mentioned the idea of reevaluating coverage. When and how often should this be done?

Answer: There are two types. The first is your car’s coverage. The second is the auto insurance company you choose. It is not a common market for auto insurance. Advertising is more important than price to compete in the auto insurance market. We see Geico, Progressive, State Farm, and all the other companies battling it out with funny characters, athletes, and telling us how great their products are. Prices can vary widely depending on which market they are in and what zip code you reside in. I would recommend that you review your insurance policy every two to three years.

Reevaluate your insurance coverage

Its best to reevaluate your coverage when you are looking for a company. You don’t need collision coverage if your car’s worth has dropped. This means you may need to increase or decrease your liability coverage depending on how your personal financial situation has changed. If you have lost your job or have lost assets, then you may not have enough assets to reduce your liability coverage and save money.

You may also want to increase your liability coverage if you have more assets. Consider whether the coverage you currently have is sufficient to protect your wealth.

Devices and Discounts

Question: We will be discussing discounts as well as auto insurance company-provided devices that monitor driving habits and mileage. Let’s start with discounts.

Answer: Sure. There are several types of discounts. Some discounts are reasonable, like credit for safe driving and having no accidents. If you stay with a company for a while, some companies will offer a discount. It’s called a loyalty discount. Another discount is a multi-vehicle discount. This makes sense since most people won’t insure the same car with both companies.

Discounts and bundling

A lot of companies offer multiline discounts. This is a great deal. It bothers me as a consumer advocate because if your homeowners insurance is bundled with your car insurance, then you will get a discount. A person who doesn’t have a home will pay more for car insurance, and you’ll be paying for the discount. It is worth asking about bundling and multi-vehicle insurance. This is especially true if you’re thinking of buying life insurance, or any other type of insurance.

You’ll also hear it from me and my colleagues in consumer advocacy. Insurance companies give discounts to people for things that do not have to do with driving. For example, auto insurance companies may offer discounts to engineers, architects, doctors, and lawyers. They can also make healthcare workers, janitors, and cashiers pay more.

Other discounts

A college degree can be used to get a discount. However, they will charge surcharges for high school graduates. Another factor is your credit score. Companies will charge less if you have high credit scores than if your credit is fair or poor.

Others are lesser-known. If you’re married, some companies offer a discount. These same companies will charge you more if your spouse is unable to work. This is called a widow penalty. A good student discount is available, which can prove to be very helpful for young drivers, as they are usually more costly to insure. A “student away at home” discount is also available. You may be eligible for a discount if your child lives 100 miles from home while attending college.

Devices provided by insurers

Question: Okay. But what about devices provided by insurers that track your driving habits?

Answer: The issue of telematics devices is fluid for consumers. Telematics is based on the notion that technology can allow auto insurance companies to assess your driving habits and determine your riskiness. These include things such as how often you drive and other factors. These are just a few of the many reasons why accidents can occur.

We can monitor your driving and offer you a better rate if your safety is on the road. We’re riding shotgun alongside you. Some people aren’t happy with the idea that insurance companies literally monitor their every move. Some people don’t like the idea that auto insurance companies know where they are going and what time they drive.

These devices are not yet the majority in the market. They are only used by a small number of customers. They are still not fully proven. This is also due to auto insurance companies not being completely transparent about the information they collect and how it relates to their rates.

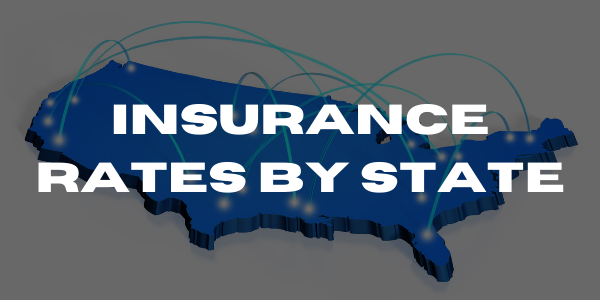

Auto insurance rates by state

| State | Minimum liability coverage limits (in thousands) | Average annual cost of minimum coverage | Average annual cost of full coverage |

|---|---|---|---|

| Alabama | 25/50/25 | $469 | $1,623 |

| Alaska | 50/100/25 | $373 | $1,559 |

| Arizona | 25/50/15 | $555 | $1,547 |

| Arkansas | 25/50/25 | $470 | $1,914 |

| California | 15/30/5 | $733 | $2,065 |

| Colorado | 25/50/15 | $518 | $2,016 |

| Connecticut | 25/50/25 | $794 | $1,845 |

| Delaware | 25/50/10 | $787 | $1,775 |

| Florida | 10/20/10 | $1,101 | $2,364 |

| Georgia | 25/50/25 | $756 | $1,982 |

| Hawaii | 20/40/10 | $354 | $1,127 |

| Idaho | 25/50/15 | $307 | $1,045 |

| Illinois | 25/50/20 | $442 | $1,485 |

| Indiana | 25/50/25 | $367 | $1,254 |

| Iowa | 20/40/15 | $252 | $1,260 |

| Kansas | 25/50/25 | $410 | $1,698 |

| Kentucky | 25/50/25 | $748 | $2,128 |

| Louisiana | 15/30/25 | $975 | $2,724 |

| Maine | 50/100/25 | $294 | $965 |

| Maryland | 30/60/15 | $767 | $1,877 |

| Massachusetts | 20/40/5 | $510 | $1,223 |

| Michigan | 50/100/10 | $948 | $2,309 |

| Minnesota | 30/60/10 | $537 | $1,643 |

| Mississippi | 25/50/25 | $492 | $1,782 |

| Missouri | 25/50/25 | $468 | $1,661 |

| Montana | 25/50/20 | $342 | $1,737 |

| Nebraska | 25/50/25 | $335 | $1,531 |

| Nevada | 25/50/20 | $860 | $2,245 |

| New Hampshire | 25/50/25 | $389 | $1,275 |

| New Jersey | 15/30/5 | $847 | $1,757 |

| New Mexico | 25/50/10 | $385 | $1,419 |

| New York | 25/50/10 | $1,062 | $2,321 |

| North Carolina | 30/60/25 | $413 | $1,325 |

| North Dakota | 25/50/25 | $285 | $1,264 |

| Ohio | 25/50/25 | $328 | $1,034 |

| Oklahoma | 25/50/25 | $423 | $1,873 |

| Oregon | 25/50/20 | $610 | $1,346 |

| Pennsylvania | 15/30/5 | $427 | $1,476 |

| Rhode Island | 25/50/25 | $749 | $2,018 |

| South Carolina | 25/50/25 | $558 | $1,512 |

| South Dakota | 25/50/25 | $275 | $1,642 |

| Tennessee | 25/50/15 | $371 | $1,338 |

| Texas | 30/60/25 | $524 | $1,823 |

| Utah | 25/65/15 | $528 | $1,306 |

| Vermont | 25/50/10 | $292 | $1,207 |

| Virginia | 30/60/20 | $441 | $1,304 |

| Washington | 25/50/10 | $463 | $1,176 |

| Washington, D.C. | 25/50/10 | $704 | $1,855 |

| West Virginia | 25/50/25 | $458 | $1,499 |

| Wisconsin | 25/50/10 | $332 | $1,186 |

| Wyoming | 25/50/20 | $271 | $1,495 |

What about my privacy

The privacy issue and what companies do to the data they collect is another concern. Is it possible for them to sell the data so that a local market can see we pass there four times per week? People trust that the data is used only to assess riskiness.

This is akin to sitting at a fork in the road. The question is, will the state regulators and auto insurance companies ensure that this product not only encourages safe driving but also protects consumers against corporate abuses? Or will it just be another way for companies to get into our lives and extract data they can monetize?

We hope that the regulators and legislators will ensure that these potentially valuable products are available to all and that there are discounts for them.

Consumer Protection

Question: Last but not least, there is the matter of consumer protection in auto insurance. What options do you have if you feel the auto insurance company made a mistake when you filed a claim against your auto policy?

Answer: There are many options if you’re involved with a claim that isn’t right. You can appeal to the company. You can also go to civil courts.

The state insurance departments have consumer complaint mechanisms that offer varying degrees of relief. California has a customer complaint team that includes people who are experts in the field. Even this will only take you so far.

My view is that regulators could improve their performance. This is not to say that consumers shouldn’t be forced to wait for something to go wrong. The only product that the government requires us to purchase in America is auto insurance. A car is essential for most people to get to work. We lack the infrastructure to support people who have good jobs and don’t need a vehicle.

It is a compulsory purchase. This private-sector product is unique and we are all required to buy it by the government. In this regard, lawmakers and regulators have a special responsibility to ensure that the supply side, which is the auto insurance companies, acts appropriately. There is still a lot of work to do on the front. We do have a resource for consumers.